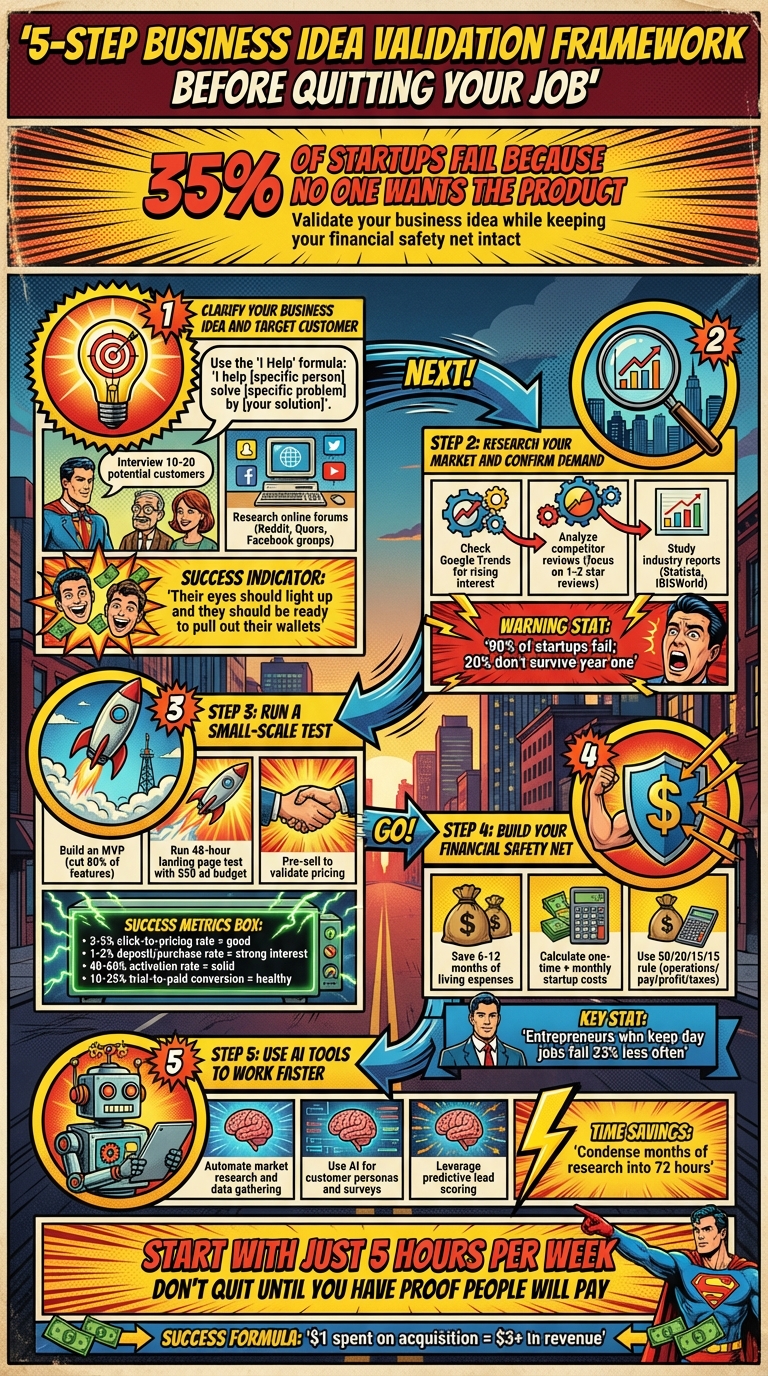

How to Validate Business Ideas Before Quitting Your Job

If you’re thinking about leaving your job to start a business, don’t make the mistake of diving in without testing your idea first. Over 35% of startups fail because no one wants the product. Instead of gambling your savings, follow these steps to validate your business idea while keeping your financial safety net intact:

- Test Demand: Create a simple landing page or pre-sell your product to see if people will pay for it.

- Research Your Market: Use tools like Google Trends and competitor reviews to confirm there’s a real need.

- Talk to Customers: Interview potential buyers to understand their pain points and willingness to pay.

- Start Small: Build a basic version of your product (MVP) and test it with a small audience.

- Stay Financially Secure: Save 6–12 months of living expenses and grow your business as a side hustle before quitting.

5-Step Business Idea Validation Framework Before Quitting Your Job

Step 1: Clarify Your Business Idea and Target Customer

Narrow Down Your Business Concept

The first priority? Focus on solving a real problem, not rushing to build features or solutions. Dr. Greg Watson, a seasoned entrepreneur and professor, puts it this way:

"Fall in love with the problem, not the solution".

Ask yourself: Is my idea a vitamin or an aspirin? Vitamins are "nice-to-have" products that improve life over time, while aspirins solve urgent, immediate pain points. Aspirins are much easier to sell, especially when you’re starting out.

To refine your business idea, try the "I Help" formula: "I help [specific person] solve [specific problem] by [your solution]." For example, "I help freelance graphic designers track quarterly tax payments to avoid IRS penalties." The more specific you are, the better your chances of success. Nancy Twine, founder of Briogeo, spent nearly three years researching market trends at a small business library in New York before launching her clean beauty brand. She emphasized the importance of understanding the market:

"I wanted to make sure that I was launching in an industry that was growing and that had a large addressable market so that I had people to sell my products to".

Her preparation paid off – Briogeo grew into a multimillion-dollar company. Similarly, JJ Follano, co-founder of Zero Waste Store, used SEO tools to identify that "zero waste store" was being searched 10,000 to 15,000 times per month. After rebranding from "Earthy Shop", their sales skyrocketed from $6,000 in year one to $2 million in year two.

Once you’ve honed your concept, it’s time to pinpoint exactly who needs it.

Ready to leave the job you hate and find the fastest path to online wealth? Learn the best asset you have right now to leverage income and build financial run way in my bestseller "Fire Your Boss." Click here to download the book for free.

Define Your Target Customer

After refining your idea, shift your focus to identifying the specific group of people who will pay for it. Avoid casting too wide a net – trying to appeal to "everyone" is a fast track to wasted resources. Instead, target an underserved group facing a clear, pressing problem.

Start with online research. Platforms like Reddit, Quora, and Facebook groups are treasure troves of unfiltered complaints. Pay close attention to how people describe their frustrations – this language will later inform how you start copywriting for your marketing materials. Additionally, dig into competitor reviews on sites like Amazon, G2, or Capterra. The 1-star and 2-star reviews are especially useful for uncovering gaps in existing solutions.

But don’t stop there. Talk to real people. While friends and family may sugarcoat their feedback, potential customers won’t. Cold-email 10–20 individuals who fit your target audience and ask for a quick 10-minute conversation about their pain points. If they respond, that’s a strong indicator the problem resonates. During these interviews, use open-ended questions like "What’s the most frustrating part of this process?" or "What have you tried to fix it?".

Take a page from Webb Brown and Ajay Tripathy, founders of Kubecost, who interviewed over 120 teams before building their product. They looked for one key sign:

"When talking to potential customers, their eyes should light up. They should be engaged in the conversation and ready to pull out their wallets on the spot".

That kind of enthusiasm is your green light to move forward.

Step 2: Research Your Market and Confirm Demand

Now that you’ve outlined your ideal customer, it’s time to ensure there’s enough demand to support your idea. Skipping this step could mean investing in something no one actually needs.

Review Market Trends

Start by using tools like Google Trends and Moz to check if interest in your idea is growing, stable, or declining. A rising trend indicates demand, while stagnant or falling interest should make you pause and reassess.

Dive into industry reports from sources like Statista, IBISWorld, or the U.S. Census Bureau to understand market size and growth potential. Using NAICS codes can help you standardize your research, making it easier to compare data across different sources.

Social media platforms and forums like Reddit, LinkedIn, and Quora are goldmines for spotting unmet needs. Look for recurring complaints or problems that your solution could address. Tools like TrendFeedr can also speed things up by analyzing patent filings, startup investments, and R&D activity to identify areas ripe for innovation.

Here’s the harsh truth: around 90% of startups fail, and over 20% don’t survive their first year. Many of these failures happen because founders skip the research and create products no one wants. Think of market research as your safety net – it’s not optional.

Once you’ve confirmed there’s demand, it’s time to analyze the competition.

Examine Your Competitors

Identify your competitors and sort them into three groups: direct (same product, same audience), indirect (different solution to the same problem), and potential (businesses that could pivot into your space). For each competitor, evaluate their product features, pricing, marketing strategies, and customer experience.

A quick way to find opportunities is by studying negative reviews on platforms like G2, Capterra, or Yelp. These often highlight what customers find frustrating about current solutions. You can also sign up for competitor newsletters, test their free trials, or even buy their products to experience their customer journey firsthand.

Want to predict a competitor’s next move? Check their LinkedIn job postings. For example, hiring for roles like "Head of Expansion" or "AI Engineer" might hint at their upcoming strategies. You can also estimate their revenue by multiplying their employee count by $150,000 for well-funded companies or $200,000 for leaner ones.

Jessica McKellar, co-founder of Pilot, offers a key piece of advice:

"Build your startup in the biggest possible market because you can’t change it later. It’s like building a house: location can’t change."

If your research reveals a small, stagnant market dominated by established players, it might be wise to rethink your approach before diving in.

Once you’ve mapped out the competition, the next step is to validate your findings with direct input from potential customers.

Collect Customer Feedback

Talk to potential customers – but avoid friends and family. They’re likely to tell you what you want to hear, not what you need to know. Use open-ended questions like, “What’s the most frustrating part of this process?” to uncover genuine pain points.

To test demand on a larger scale, try a "smoke test." Create a simple landing page that describes your product and includes a call to action, such as “Join the Waitlist” or “Pre-Order Now.” Use social media ads or niche forums to drive traffic to the page, and track how many people engage. A healthy click-to-pricing rate is 3–5%, while a 1–2% purchase or deposit rate indicates solid interest.

For example, in 2021, Waterboy co-founders Mike Xhaxho and Connor Saeli built an SMS list of 18,000 to 20,000 leads before launching their hydration brand. Their first production run sold out in just one hour. Similarly, in 2019, Bola Grills founder David Levy used an Indiegogo campaign to validate his idea, raising $22,000 in 30 days and selling 94 grills before starting full-scale production.

Sunita Mohanty, former Product Lead at Meta and Oculus, sums it up perfectly:

"The bottom line is that you can very easily build something, but to increase your chance of creating something that is solving a real problem you need to be more rigorous in your approach."

Taking the time to validate now can save you from costly mistakes down the road.

Step 3: Run a Small-Scale Test of Your Idea

You’ve got an idea – but will people actually pay for it? That’s the real question. Before you make any big moves (like quitting your job), you need to test your idea with minimal time and money. The goal isn’t perfection; it’s to prove your core assumption while keeping risks low.

Create a Minimum Viable Product (MVP)

An MVP is the simplest version of your product that still delivers value. The trick? Don’t overdo it. As Gagan Biyani, co-founder and CEO of Maven, puts it:

"An MVT… does not attempt to look like the eventual product. It’s rather a specific test of an assumption that must be true for the business to succeed."

Focus on testing what Biyani calls the atomic unit – the smallest thing you’re offering. For Google, that’s a single search query. For a meal delivery service, it’s delivering one meal. Start by listing all the features you dream of, then cut out 80% of them. Your MVP should do just one thing really well.

You don’t even need to build software right away. Try manual validation methods like:

- Concierge MVP: Deliver your service manually to test demand.

- Wizard of Oz MVP: Fake automation while doing the work manually behind the scenes.

For example, Gagan Biyani and Sam Parr tested their course platform idea by running a single cohort-based course. Without building any software, they made over $150,000 in revenue and got a 9/10 student rating. Similarly, Airbnb’s founders tested their idea by renting out their own apartment and creating a bare-bones website. They found paying guests almost immediately.

If you need a digital prototype, use no-code tools. For instance, Carrd lets you build simple landing pages for just $9 per year. The key is speed: instead of spending $80,000 and six months on a full app, you can test your idea in 48 hours for $300–$500.

Once your lean MVP is validated, it’s time to test the waters with small-scale launches.

Launch Small Tests

With an MVP in hand, the next step is to validate pricing and demand. The fastest way? Pre-sales. Ask customers to commit payment before the product exists.

Here’s how you can do it:

- 48-hour test: Create a landing page in two hours with a headline that addresses the problem you solve. Use a small ad budget – around $50 for Google or Facebook Ads – to drive traffic. Include a clear call-to-action like "Join the Waitlist" or "Pre-Order Now."

- Direct outreach: Email your network offering a limited number of pre-orders at a set price. This gauges immediate interest and demand.

Take Ryan Robinson’s approach as an example. In December 2016, he ran a 30-day validation challenge for a book idea. With less than $500, he pre-sold 12 copies, made $108 in revenue, and built an email list of 565 interested subscribers – all before writing a single chapter.

When reaching out, focus on specifics. Ask potential customers how they currently solve the problem and what they’ve paid for similar solutions in the past. This is far more reliable than asking if they "would" buy your product.

Another option is to run limited pilot programs with a small group of early adopters. These pilots provide real-world feedback without overcommitting. The "100/1,000 rule" suggests executing 100 marketing actions and talking to 1,000 people to gather enough feedback.

Track Results and Key Metrics

Don’t rely on guesses – track measurable results. Focus on actionable metrics that guide your decisions, not vanity metrics like pageviews or follower counts.

Here’s what healthy early-stage numbers might look like:

- 3–5% click-to-pricing rate on qualified traffic is a good sign.

- 1–2% deposit or Letter of Intent (LOI) rate signals strong interest for many B2B offers.

- For simple tools, a 40–60% activation rate (users hitting "first value" within seven days) is solid.

- Trial-to-paid conversion rates for SMB tools typically fall between 10–25%.

Use this framework to interpret your landing page results:

| Signups | Calls Booked | What It Means |

|---|---|---|

| 0–5 | 0–1 | Scrap it; no demand |

| 5–20 | 2–3 | Pivot; test different value proposition |

| 20–50 | 4+ | Validate pricing; create paid pilot |

| 50+ | 10+ | Build it now; ship MVP in 4 weeks |

Set success thresholds before running the test to avoid falling into the trap of founder bias.

Pay attention to what users do, not just what they say. Tools like heatmaps and session recordings can show how people interact with your prototype. If your conversion rate drops, conduct 1:1 interviews to understand why.

As Gagan Biyani wisely says:

"You’re nothing until you have customers who want your product."

Don’t invest heavily until you know your numbers. A clear path where every $1 spent on acquisition generates $3 or more in revenue is a strong indicator you’re on the right track. Remember, around 35% of startups fail because there’s no market need. Proper validation ensures you won’t be part of that statistic.

Step 4: Build Your Financial Safety Net

You’ve confirmed there’s a demand for your idea – now it’s time to get your finances squared away. Here’s the reality: 20% of startups fail within their first year. And if you’re living off savings, that pressure can feel unbearable. Before you walk away from your current paycheck, you need a solid financial plan in place.

Calculate Your Startup Costs

Start by breaking down your expenses into two categories: one-time costs and monthly costs. One-time costs might include things like licenses, permits, initial equipment, logo design, and setting up your website. Monthly costs, on the other hand, cover recurring expenses like rent, utilities, insurance, software subscriptions, marketing, and salaries. Write everything down – be as specific as possible.

| Expense Type | Common Examples |

|---|---|

| One-Time Costs | Licenses, permits, logo design, initial equipment, website setup, legal fees |

| Monthly Costs | Rent, utilities, salaries, insurance, marketing, software subscriptions |

Plan for at least a year’s worth of monthly expenses – five years is even better for a broader view. If you’re unsure about certain costs, reach out to mentors, vendors, or service providers for accurate estimates. And here’s a big one: keep your business and personal expenses completely separate from day one.

Ready to leave the job you hate and find the fastest path to online wealth? Learn the best asset you have right now to leverage income and build financial run way in my bestseller "Fire Your Boss." Click here to download the book for free.

Next, figure out your personal runway – how long your savings will last before you’re out of money. This step is critical. Make sure you have enough savings to cover both your personal and business expenses before leaving your current job.

Save an Emergency Fund

The general rule is to save 6–12 months of living expenses before taking the plunge. This cushion gives you the freedom to test and grow your business without panicking over how to pay rent. Calculate your personal living costs along with your business expenses for at least a year.

Interestingly, entrepreneurs who keep their day jobs while launching a business fail 33% less often than those who quit immediately. Your job isn’t just a paycheck – it’s a safety net that allows you to experiment without the pressure of needing instant profitability.

If possible, secure some actual revenue before quitting. Michael Taylor, for instance, didn’t leave his job until he had locked in $20,000 in recurring revenue for Ladder. He solved a specific problem, offered a 20% money-back guarantee, and ensured cash flow before taking the leap. Once you’ve built your emergency fund, reinvest any revenue to fuel steady growth.

Grow Your Business Gradually

Don’t rush to scale. Use the 50/20/15/15 rule to allocate your revenue wisely: 50% for operations, 20% for your own pay, 15% for profit, and 15% for taxes. This approach keeps your finances stable and prevents you from draining personal savings to keep things running.

Reinvest the "profit" portion back into the business – like paying off one-time capital expenses – rather than dipping into your personal income. Gabe Arnold, founder of Copywriter Today, offers this advice:

"If you can’t make the numbers work [at the 50% operating expense level] then you have one of two options available: Adjust your pricing or scrap the idea."

Finally, hold off on major investments in scaling until you’ve figured out a formula where every $1 spent on customer acquisition brings in $3 or more in revenue. By growing gradually, you can manage costs and avoid unnecessary debt.

Step 5: Use AI Tools to Work Faster and Smarter

When you’re juggling a full-time job and testing the waters of a startup, time becomes your most valuable resource. AI tools can drastically reduce the time needed for tasks that used to take weeks or even months. With the right tools, you can condense months of traditional research into just a few days – sometimes as little as 72 hours. This isn’t about working harder; it’s about working smarter.

Automate Repetitive Tasks

Repetitive tasks can drain your energy and eat up your precious free time. AI tools can step in to handle these for you. Instead of manually digging through competitor websites or analyzing social media trends, AI can automatically gather and process market data, including consumer behavior patterns and your competitors’ strategies. Want to create customer personas or map out user journeys? Generative AI can do that too – what once took weeks can now be done in a matter of hours. These tools free you up to focus on strategy and decision-making, rather than getting bogged down in busywork.

Improve Your Marketing and Outreach

AI isn’t just about saving time – it’s also about boosting results. Tools like ChatGPT can help you brainstorm product ideas, create detailed user personas, and draft research surveys or marketing messages. On top of that, predictive lead scoring tools can rank potential customers based on how likely they are to convert. This means you can prioritize your efforts on the leads that matter most, increasing the chances of turning them into loyal customers. These AI-driven tools can give your marketing efforts a serious edge.

Learn AI Methods with Serve No Master

For anyone looking to build a location-independent and automated business, Serve No Master is a great place to start. Created by bestselling author Jonathan Green, this platform offers courses designed to teach professionals how to use AI for business automation, content creation, and digital product development. The goal? To help you create passive income streams while still holding down a full-time job. The free "ChatGPT Profits" book is an excellent starting point, offering 25 actionable ways to use ChatGPT, along with step-by-step instructions for crafting effective prompts. It’s a practical resource for anyone ready to validate ideas faster and transition smoothly from corporate life to entrepreneurship.

Conclusion: Start Validating Your Idea Today

The line between a thriving business and one that never gets off the ground often comes down to one thing: testing your idea before diving in. Did you know that 35% of startups fail because there’s no market need for their product or service? You don’t have to be part of that statistic. By following the steps we’ve outlined – defining your idea, researching demand, testing with a minimum viable product (MVP), securing financial stability, and using AI tools – you can increase your chances of success while keeping the security of your paycheck.

"An untested idea is just a hypothesis – and building a business on an untested hypothesis is like constructing a house on sand." – Dr. Greg Watson, Serial Entrepreneur and Professor

This quote perfectly highlights why testing your idea is essential. It’s about taking small, calculated steps toward validation before committing fully.

Start small. Dedicate just five hours a week. That could mean carving out an hour each evening or setting aside a Saturday morning. Entrepreneurs like Ryan Robinson and Michael Taylor prove that minimal investments can yield big insights. Robinson spent less than $500 over 30 days, pre-sold 12 copies of his product, earned $108, and grew an email list of 565 – all without leaving his full-time job. Meanwhile, Taylor secured $20,000 in recurring revenue by offering a 20% money-back guarantee to startup founders, even before creating a website.

The key is to focus on measurable sales outcomes. Instead of spending months perfecting a product, aim to secure initial revenue early. Tools like those from Serve No Master can speed up this process. By using AI, you can streamline market research, customer outreach, and content creation, cutting tasks that once took weeks into just days – or even hours. The free "ChatGPT Profits" book offered by the platform is a great starting point for automating these steps and validating your idea faster.

Your current job is your safety net. It funds your validation efforts and keeps you financially secure while you test the waters. Don’t quit until you’ve answered the most critical question: Will people pay for what you’re offering? Once you have proof – through data, paying customers, and revenue – you can step into your new venture with confidence, not just hope.

FAQs

How can I use AI to test my business idea before leaving my job?

AI tools make it easier than ever to test your business idea without quitting your day job. These tools can analyze everything from market demand to competition, helping you figure out if your idea has legs before you dive in.

For instance, AI can simulate customer interactions to see how people might respond to your product or service. It can also assess market fit and flag potential roadblocks you might not have considered. Some platforms even include checklists or feedback systems to help you fine-tune your concept, define your audience, and ensure your idea solves an actual problem.

The best part? You can collect data, test your assumptions, and make smarter decisions – all without taking on unnecessary risks or putting your current job on the line. AI gives you the tools to validate your idea quickly and with minimal effort.

What are the signs that my business idea has real market demand?

To figure out if your business idea has real market demand, focus on finding proof that people are interested and willing to pay. This could mean getting pre-sales, landing your first paying customers, or creating a list of potential buyers who are genuinely excited about what you’re offering.

You should also back up your idea with market research and real-world testing. Run surveys, ask for feedback directly from potential customers, or launch a small, test version of your product or service. If your audience consistently shows interest and is prepared to spend money, you’ve got a solid sign that demand exists.

How can I test my business idea without risking my financial stability?

Testing a business idea while keeping your finances steady comes down to smart decisions and careful planning. One of the best ways to do this is by holding onto your full-time job while you test the waters. This approach lets you experiment with your idea without putting your main income at risk. To validate your concept, stick to affordable methods like building a minimum viable product (MVP), running small online ads, or even conducting customer interviews to see if there’s real interest.

Another key step is creating a financial cushion before you start. Setting aside savings to cover your personal expenses can ease the pressure and give you some breathing room. You might also want to explore pre-selling your product or service. This way, you can gauge demand without needing a large upfront investment. By juggling your job, keeping your finances in check, and testing your idea with care, you can move forward with confidence while keeping financial risks to a minimum.

Related Blog Posts

- 7 Ways to Make Money Online With No Experience

- How to Start a Side Hustle While Working Full Time

- Freelancing vs Starting a Business: Which Is Right?

- How ChatGPT Helps Identify Profitable Niches

Ready to leave the job you hate and find the fastest path to online wealth? Learn the best asset you have right now to leverage income and build financial run way in my bestseller "Fire Your Boss." Click here to download the book for free.